Most men and women look at life insurance as a means of replacing their income stream when they die to support their surviving loved ones financially. Then again, it is not always about loss of an income stream. Since burials and funerals typically cost a lot more than most folks assume they do, it is essential to comprehend solutions like Final Expense insurance.

After all, the actual purpose of life insurance is making certain your loved ones are financially taken care of after you pass away and don’t have to alter their lifestyle dramatically. To be confronted with unexpected expenses after your death could undoubtedly get in the way.

There are certainly many options for obtaining life insurance coverage; each has distinct advantages and disadvantages. Not every single individual requires the substantial coverage that many life insurance policies offer. For some of those individuals, final expense insurance could very well be the ideal option, but there are generally multiple different aspects that you ought to think about when you’re searching for life insurance.

What are Final Expenses Anyway?

Simply put, your final expenses are the costs that are associated with services you required just before and immediately after you passed away. These expenses generally include the costs of your funeral and burial (or cremation), unpaid nursing home bills, unpaid medical bills (copayments and coinsurance), and any of your debts that could be transferred to your spouse or other surviving loved ones.

In most cases, the cost of the funeral, cemetery plot, and burial will be the most expensive. Most people simply don’t understand the current costs of burying a loved one. Just take a few minutes and visit some online funeral estimate services provided by Parting.com, Everplans.com, and BurialPlanning.com.

Spending just a little time and doing some online footwork will typically open the eyes of any consumer about how the cost of dying has increased over the last twenty years. There is a silver lining however, consumers can actually shop for their funeral service and negotiate the prices down. This funeral shopping was very rare in the past because shopping a half-dozen funeral homes before you buried a loved one seemed rather tasteless.

It’s a little more difficult to predict non-funeral expenses like unpaid nursing home expenses or outstanding debt unless you have a pretty good idea when your passing will take place. Most people do admit, however, the funeral expenses were much higher than they anticipated and pretty much consumed the majority of the policy’s death benefit.

The important thing here is that you don’t want to leave the cost of your funeral to your family and friends. You want to take care of these costs in advance, and final expense insurance is the most affordable method to do that.

Should I use Term or Whole Life for My Final Expense Insurance Policy?

The short answer is “it depends.” There are pros and cons to each type of insurance product when you consider why you are using it. Term life insurance is certainly less expensive than whole life insurance (that’s a pro), but there are some drawbacks:

- Term insurance is temporary, and you can easily outlive your insurance policy

- The most affordable term insurance generally requires a lot of medical questions, a medical exam, and a blood and urine analysis.

- Term life insurance can be more difficult to qualify for, especially if you are over fifty and have some medical issues.

Whole life insurance is the foundation that most final expense insurance policies are built on, and there are several reasons why:

- Whole life is permanent insurance and will stay in force for life as long as the premiums are paid. It is guaranteed.

- The periodic premiums for a whole life policy cannot be changed by the insurer once the policy is issued. The premiums will not go up as you get older or if you become ill.

- Whole life insurance builds cash value over the life of the policy which is available to the policyholder through policy loans. If you have an emergency and need some quick cash, your cash value is like a bank, and you have the keys.

- Whole life final expense insurance generally never requires a medical exam and can be issued very quickly with little to no underwriting aggravation.

How much is My Final Expense Insurance Going to Cost?

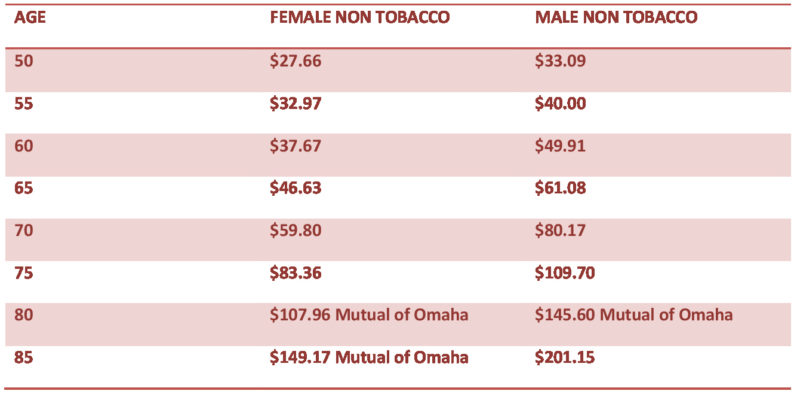

We can’t certainly help with that. As an independent insurance broker, Docktor’s Insurance represents the top-rated insurance companies that offer Final Expense Insurance. In fact, we have listed below the best rates for $11,000 Final Expense Insurance.

Please review the following assumptions before you review our rate chart:

Rates are based on $11,000 final expense insurance coverage

- Rates are based on non-smokers. Those who smoke will pay a lot more insurance premiums.

- The monthly rates are determined by your age group. For a quote based on your exact age, simply fill out our instant quote form.

- We represent many highly-rated life insurance companies but feel this selection will provide an accurate picture of the premium you can expect to pay.

![]()

As you may have noticed, we listed rates from Mutual of Omaha in the 80 and 85-year-old age group because the rates are more competitive. This is one of the many perks of shopping with an independent agent who represents multiple insurance companies. These rates are for insurance with a level benefit that provides first-day coverage.

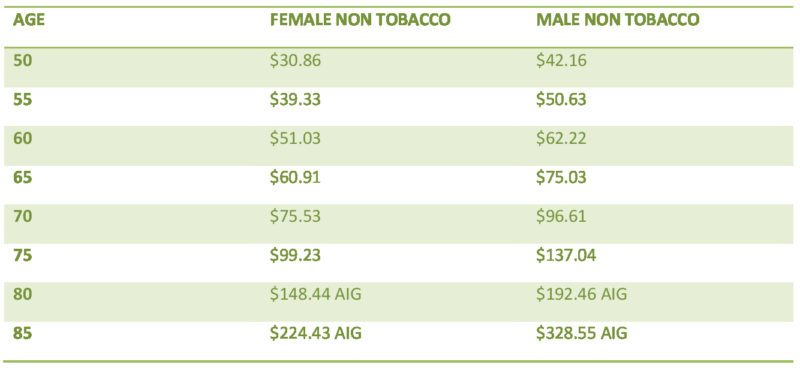

Can I be Declined?

Although final expense insurance policies do not require a medical exam or blood and urine tests, you can be declined based on the answers you provide to the health questions on the application. In this case, Docktor’s Insurance will recommend guaranteed issue life insurance and we have provided the rates below.

As you will notice, the rates for guaranteed issue life insurance are considerably higher than the level benefit final expense insurance. Since a guaranteed issue policy does not take any health information into consideration, the insurer is accepting an unknown health risk and will charge more for the riskier applicant.

There are other caveats that you should be aware of with guaranteed issue insurance, so be sure and speak with one of our insurance professionals so you can make an informed decision.